The global economy is past the point of being able to avoid a sharp recession, warns the watchdog of the global financial system. The IMF World Economic Outlook was released this week, forecasting that global real gross domestic product (GDP) will slow sharply in 2023. A hard landing is now expected, with advanced economies likely to get hit the worst. The agency hasn’t shared such a weak medium-term forecast since Law & Order was first aired.

The weak economy in 1990 had nothing to do with Law & Order, just highlighting how long ago it was. Dun dun.

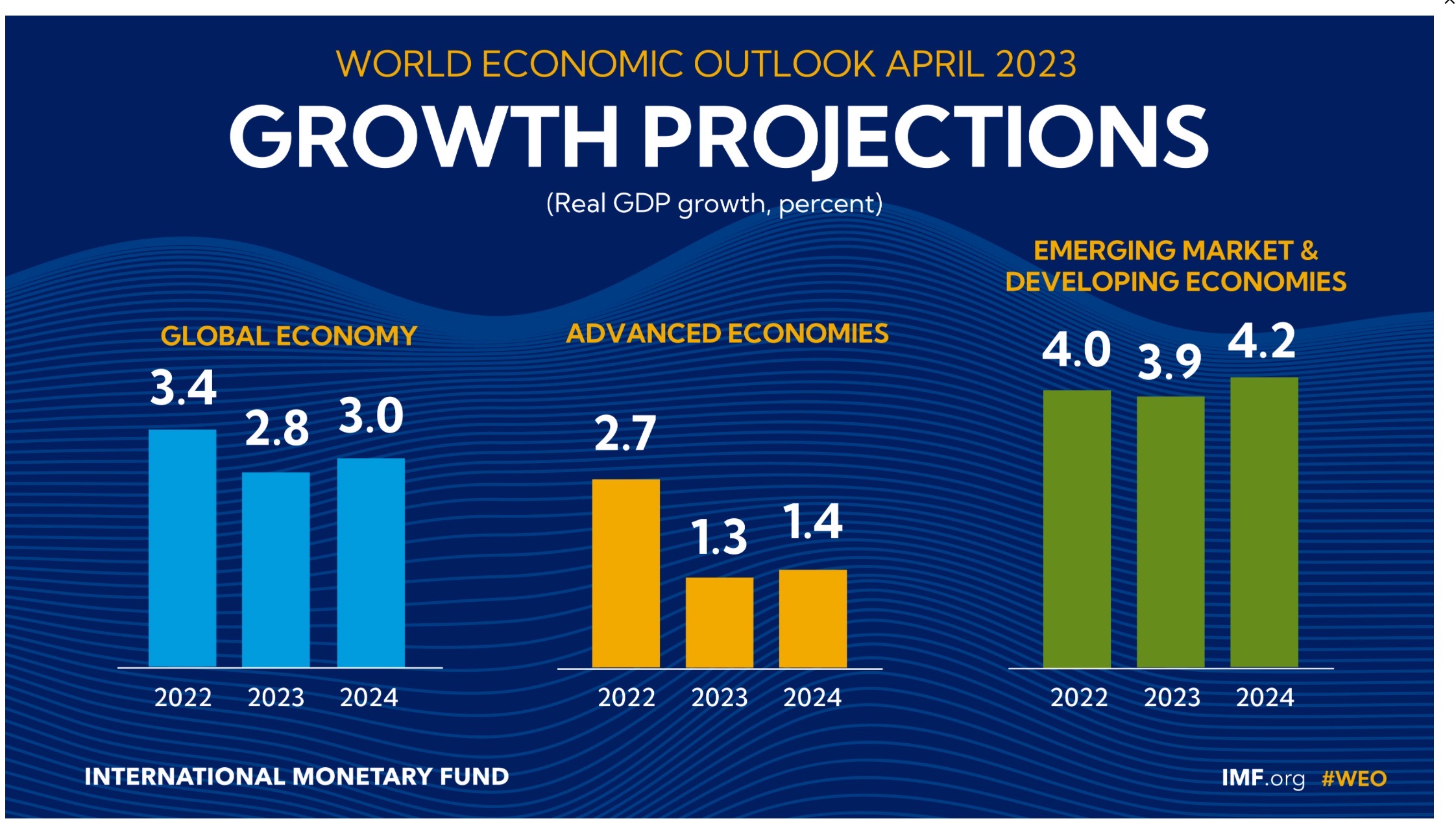

The Global Economy Is Heading For A Hard Landing

A soft landing for the global economy is now unlikely, according to the latest IMF forecast. “Tentative signs in early 2023 that the world economy could achieve a soft landing—with inflation coming down and growth steady—have receded amid stubbornly high inflation and recent financial sector turmoil,” said the agency.

Source: IMF.

Global real GDP growth is forecast to fall from 3.4% growth in 2022, to just 2.8% in 2023. Next year a mild bounce is expected to push growth back to 3.0%, but it appears to be a plateau. They note the same level of growth is expected 5-years down the road as well. “… The lowest medium term forecast in decades,” reads the forecast notes.

High Inflation Won’t Be Tamed Before 2025

The weakest GDP growth since 1990 is primarily attributed to the inflation crisis. Although inflation is moderating, it’s just not cooling fast enough and in the right places. Inflation has been primarily reduced through lower food and commodity prices, but core inflation (inflation minus those two) has been sticky. The earliest inflation is expected to moderate will be 2025, so buckle up.

Central banks have been able to achieve some success in cooling inflation. Unfortunately, higher rates have produced a mild (so far) banking crisis. As a result, they don’t see economies having the ability to keep reducing inflation via higher rates for long enough.

Global Economic Risks Are Slanted To The Downside

The IMF warns the risk is slanted to even further downside. Their baseline forecast applies if inflation is contained and the banking crisis is contained. Significant progress is being made when it comes to inflation, but bank issues are a wild card. Containment measures are working as intended, but they always do before they don’t.

If further financial sector stress can’t be contained, global real GDP falls to 2.5% growth. They see this being the worst recession since 2001, excluding the pandemic and 2009 financial crisis. It’s not clear why they chose to exclude those two events in their analysis, but they were “special” recessions with induced shocks. The forecast recession resembles a more textbook economic recession, caused by exhausted demand and leverage.

Advanced Economies To Be Hit The Hardest This Recession

Surprisingly, advanced economies are the weight on the global forecast. Real GDP growth is forecast to fall from 2.7% in 2022, to just 1.3% in 2023. Unlike the global forecast, no major bounce follows next year, inching its way to just a 1.4% increase. The G7 (+1.1%) and Euro Area (+0.8%) are the major drag on when it comes to advanced economies in the coming months.

Emerging Market & Developing Economies Will Come Out Stronger

Emerging markets and developing economies are forecast to weather this storm well. Real GDP growth is forecast to see a slight reduction from 4.0% in 2022 to 3.9% in 2023. By next year, they’re expected to bounce back even better with 4.2% growth in 2024. This is in stark contrast to how emerging and developing countries were impacted by the Global Financial Crisis and pandemic, where they were hardest hit.

Emerging and developing economies are traditionally smaller and thus easier to realize real GDP growth. Now those economies include countries like China and India, with the growth likely to improve baseline conditions towards advanced economy standards.

Policymakers will face difficult decisions in the coming months. An excess of easy money during the pandemic provided inflationary pressures on top of supply chain-related issues. Now with a new recession fast approaching, the options for softening the blow are limited. They can’t just helicopter easy money without undermining the progress made by central banks in recent months.

“A hard landing — particularly for advanced economies — has become a much larger risk. Policymakers may face difficult trade-offs to bring sticky inflation down and maintain growth while also preserving financial stability,” said the IMF.